Step Costs Strategic Cost Management Vocab, Definition, Explanations Fiveable

The concept is used when making investment decisions and deciding whether to accept additional customer orders. A step cost is a fixed cost within certain boundaries, outside of which it will change. The same pattern applies in reverse when the volume of activity declines.

Step Variable Cost: Definition, Understanding, Examples

If the shop begins receiving 31 or more customers per hour, it must hire a second employee, increasing its costs to $70 ($40 for two employees, $30 for others). Additionally, a step cost analysis can aid in optimizing production schedules, resource allocation, and capacity utilization to achieve operational efficiency. The net return or profit from the pencil example can be computed by using variable and fixed costs.

- Total variable costs are the sum of all of the costs that vary in direct proportion to production.

- When they classify costs properly, managers can use cost data to make decisions and plan for the future of the business.

- So, for decision-making purposes, costs are categorized as either fixed or variable.

- Let’s use a catering business as an example to illustrate the concept of step variable costs.

- His fixed costs still remained fixed in total and his total variable cost rose as the number of T-shirts he produced rose.

- Given the importance of step costs to the profitability of a business, it makes sense to clearly identify the activity levels at which these costs will be incurred.

Step Cost Explained

Step costs are best explained in the context of a business experiencing increases in activity beyond the relevant range. A step cost is also known as a stepped cost or a step-variable cost. If the shop receives anywhere from zero to 30 customers per hour, it will only need to pay the cost of having one employee, say $50 ($20 for the employee, $30 for all other expenses, fixed and operating).

Strategic Cost Management

The distributor charges $10 per bike for shipping for 1 to 10 bikes but $8 per bike for 11 to 20 bikes. If Bert wants to save money and control his cost of goods sold, he can order how to deduct mortgage points on your tax return an 11th bike and drop his shipping cost by $2 per bike. It is important for Bert to know what is fixed and what is variable so that he can control his costs as much as possible.

In practice, the classification of costs changes as the use of the cost data changes. In fact, a single cost, such as rent, may be classified by one company as a fixed cost, by another company as a committed cost, and by even another company as a period cost. Understanding different cost classifications and how certain costs can be used in different ways is critical to managerial accounting.

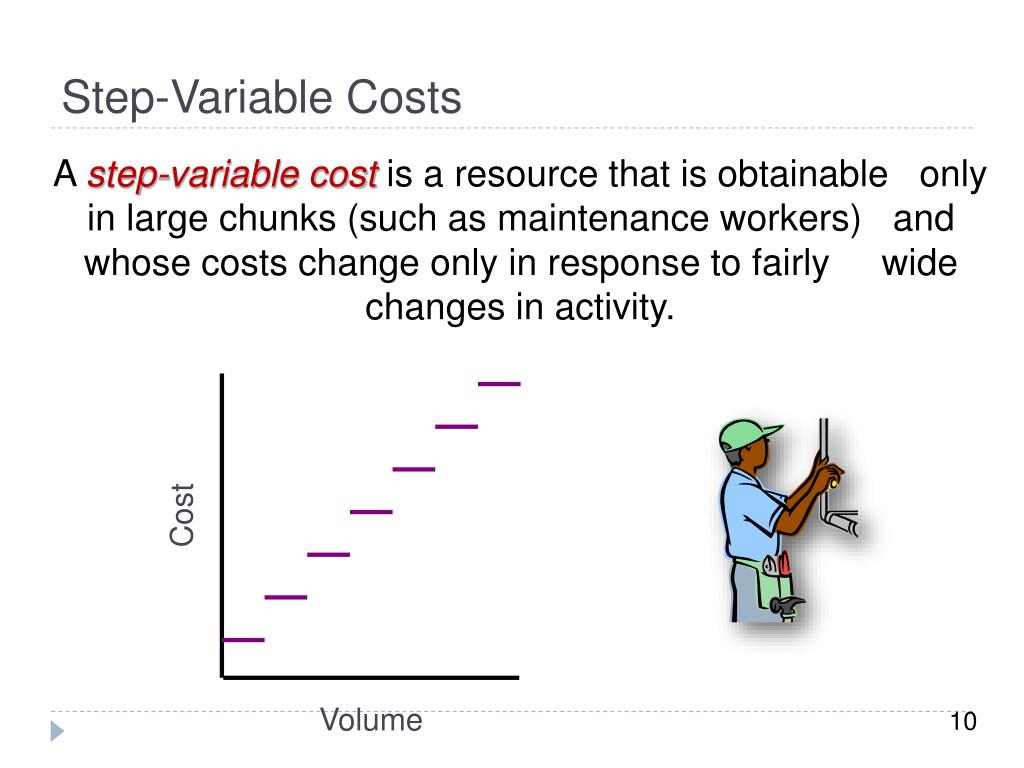

The costs will not fluctuate for a certain range of output, but will abruptly rise or fall after crossing a threshold level. When you map out step costs on a graph, they reveal a stair-step pattern. Businesses generally anticipate a certain amount of fixed or budgeted cost when activity levels remain constant over an expected range.

What happens to the AFC if they increase or decrease the number of boats produced? Remember that the reason that organizations take the time and effort to classify costs as either fixed or variable is to be able to control costs. When they classify costs properly, managers can use cost data to make decisions and plan for the future of the business.

Committed fixed costs are fixed costs that typically cannot be eliminated if the company is going to continue to function. An example would be the lease of factory equipment for a production company. These costs are variable in the sense that they can change with the level of activity, but they do so in “steps” rather than in a continuous linear manner. Costs that do not change with the level of production or sales within a relevant range. If you look at your business finances, you’ll discover that many of your expenses are examples of step costs.

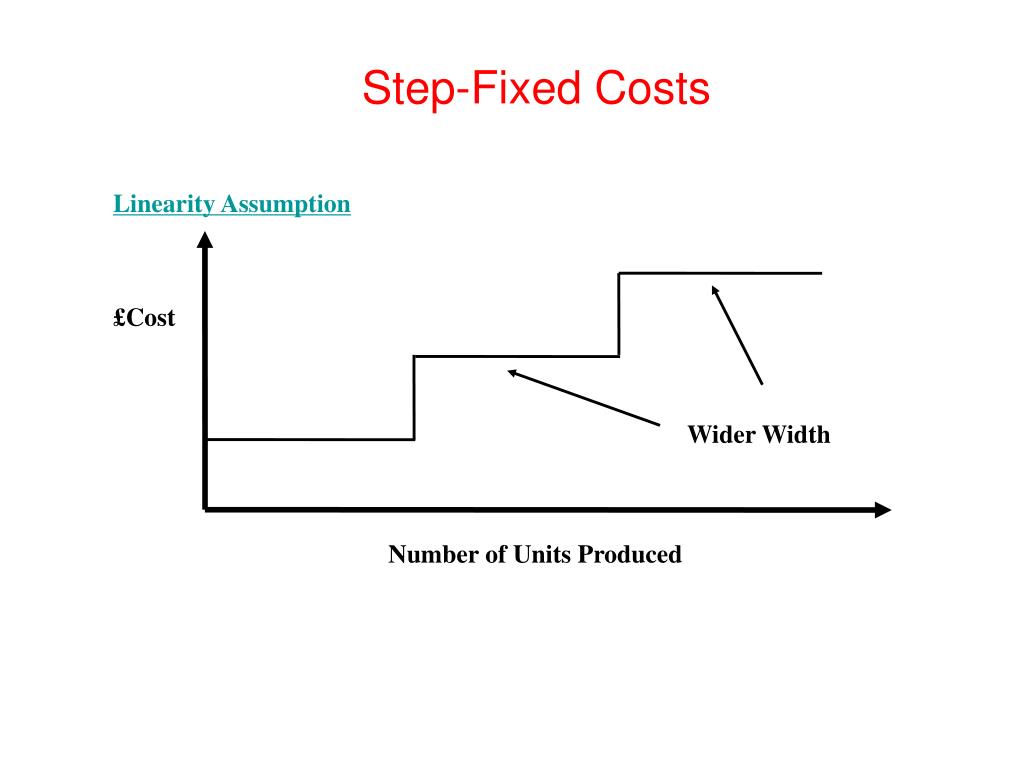

These classifications are generally used for long-range planning purposes and are covered in upper-level managerial accounting courses, so they are only briefly described here. One way to deal with a curvilinear cost patternis to assume a linear relationship between costs and volume withinsome relevant range. Within that relevant range, the total costvaries linearly with volume, at least approximately. Outside of therelevant range, we presume the assumptions about cost behavior maybe invalid. Step variable cost is also a subtype of variable cost that remains the same up to a particular level of output and increases once that particular output level is breached.

These classifications are generally used for long-range planning purposes. A second shop floor supervisor, along with additional support personnel, would be necessary if demand for the product increased to 2,001-4,000 units per day. Therefore, the total salary costs of shop floor supervisors vary with changes in product demand. It may make sense to incur higher step costs if revenue is sufficient to cover the higher cost and provide an acceptable return. If the increase in volume is relatively minor, but still calls for incurring a step cost, profits may actually decline.