The Three Parts of a Cash Flow Statement

If you’re wondering how to make a cash flow statement, these steps can guide you through the process, from gathering initial data to calculating the final cash balance. Any purchase or sale of property, equipment and plants also qualify under the investment section. The ledger accounts to review for this section include the long-term investments account, vehicles, capital equipment accounts, land and buildings. The beginning and ending balances that appear on the comparative balance sheet are the same as those in the Equipment ledger’s debit balance column on January 1 and September 12, respectively. The $10,000 credit entry is the cost of the equipment that was sold on April 3.

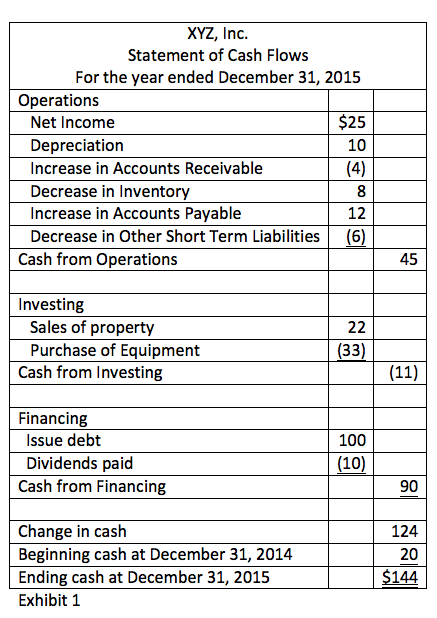

Investing Cash Flow

The cash flow statement is one of the primary financial statements used in business operations, including small businesses. Creating a cash flow statement illustrates the amount of cash the business generated during the reporting period. The cash flow statement also details the cash used during the period, helping management see where the money is going and differs. The cash flow statement consists of three primary sections plus an optional supplemental section. It shows how much money is available for your business to finance continued operations and growth.

How to Read (and Understand) an Income Statement

- The second way to prepare the operating section of the statement of cash flows is called the indirect method.

- In “Analyzing Statements of Cash Flows II,” a comparative approach is crucial for understanding cash flow trends over multiple periods.

- To opt-in for investor email alerts, please enter your email address in the field and select at least one alert option.

- The cash outflow for securities or other assets acquired, which qualify for treatment as an investing activity and are to be liquidated, if necessary, within the current operating cycle.

- Free Cash Flow was $73.3 million, compared to $67.7 million in the prior year period.

By learning how to read a cash flow statement and other financial documents, you can acquire the financial accounting skills needed to make smarter business and investment decisions, regardless of your position. Cash flow statements are powerful financial reports, so long as they’re used in tandem with income statements and balance sheets. Increase in Accounts Receivable is recorded as a $20,000 growth in accounts receivable on the income statement. Keep in mind, with both those methods, your cash flow statement is only accurate so long as the rest of your bookkeeping is accurate too. The most surefire way to know how much working capital you have is to hire a bookkeeper. They’ll make sure everything adds up, so your cash flow statement always gives you an accurate picture of your company’s financial health.

How to track cash flow using the indirect method

While companies are mostly allowed to choose any of these two methods worldwide, major accounting frameworks, like GAAPs and IFRSs, suggest the use of the direct method. We define Free Cash Flow as Cash provided by operating activities less capital expenditures, which is disclosed as Purchases of property, plant and equipment in the Company’s Consolidated Statements of Cash Flows. We use Free Cash Flow, among other measures, to evaluate the Company’s liquidity and its ability to generate cash flow. We believe that Free Cash Flow is meaningful to investors because it provides them with a view of the Company’s liquidity after deducting capital expenditures, which are considered to be a necessary component of ongoing operations.

How to Build a Statement of Cash Flows in a Financial Model

It has a net outflow of cash, which amounts to $7,648 from its financing activities. A cash flow statement (CFS) is a financial statement that captures how much cash is generated and utilized by a company or business in a specific time period. It’s important to note that cash flow is different from profit, which is why a cash flow statement is often interpreted together with other financial documents, such as a balance sheet and income statement. Based on the cash flow statement, you can see how much cash different types of activities generate, then make business decisions based on your analysis of financial statements. The purpose of a cash flow statement is to provide a detailed picture of what happened to a business’s cash during a specified period, known as the accounting period. It demonstrates an organization’s ability to operate in the short and long term, based on how much cash is flowing into and out of the business.

Analyzing changes in cash flow from one period to the next gives the investor a better idea of how the company is performing, and whether a company may be on the brink of bankruptcy or success. The CFS should also be considered in unison with the other two financial statements (see below). The operating activities on the CFS include any sources and uses of cash from business activities. In other words, it reflects how much cash is generated from a company’s products or services. Operating cash flows are calculated by adjusting net income by the changes in current asset and liability accounts.

Also, when using the indirect method, you do not have to go back and reconcile your statements with the direct method. The direct method takes more legwork and organization than the indirect method—you need to produce and track cash receipts for every cash transaction. Remember that the indirect method begins with a measure of profit, and some companies may have discretion regarding which profit metric to use. While many companies use net income, others may use operating profit/EBIT or earnings before tax.

Are you interested in gaining a toolkit for making smart financial decisions and the confidence to clearly communicate those decisions to key internal and external stakeholders? Explore our online finance and accounting can i get a tax refund with a 1099 even if i didn’t pay in any taxes courses and download our free course flowchart to determine which best aligns with your goals. The result is the business ended the year with a positive cash flow of $3.5 billion, and total cash of $14.26 billion.

The main components of a cash flow statement are cash flows from operating activities, investing activities, and financing activities. Greg didn’t invest any additional money in the business, take out a new loan, or make cash payments towards any existing debt during this accounting period, so there are no cash flows from financing activities. Under IFRS, there are two allowable ways of presenting interest expense or income in the cash flow statement. Many companies present both the interest received and interest paid as operating cash flows.